Blog

Home » Diamonds blog » ALMOST A QUARTER CENTURY AFTER DE BEERS’ LANDMARK STUDY, BRANDS COME TO DOMINATE SALES IN DIAMOND JEWELRY MARKET

Focus on

Photo by Serena T on Unsplash.com.

In the late 1990s, De Beers, which at the time controlled upward of 90 percrent of all rough diamond supply, retained the consultancy firm Bain & Company to conduct a review of its single-channel distribution system. It was a study that would eventually change the face of the diamond business.

In its report, Bain concluded that it was no longer viable or in the mining company’s interest to physically control and promote other producers’ supply of rough diamonds. Instead, Bain suggested that De Beers focus on selling and marketing its own diamonds, and so become the “Supplier of Choice” for the downstream markets.

One of the key elements of the Bain proposal was that, in the new distribution system, a clients’ supply of diamonds from De Beers should be contingent on that client’s ability to add significant value to the goods it sources, thus backing away from what essentially was the more common practice of commoditizing the product. One way of doing that, De Beers insisted, would be branding, enabling jewelry retailers to differentiate monetarily between diamonds from different suppliers. Indeed, De Beers stated in 2003 that that branding would facilitate a 50 percent increase in overall demand for diamonds by 2013.

But it would take a while. Several attempts at branding diamonds were undertaken, mainly by De Beers clients, but only a handful enjoyed any notable success. The stumbling block for most, it would appear, was that few diamond companies had the capital necessary to launch a viable diamond branding campaign.

De Beers, on other hand, did have the capital resources. It launched its Forevermark brand in 2008, pitching largely as a program that would ensure the integrity and uniqueness of high-quality individual, natural diamonds. A person acquiring a Forevermark brand stone could be guaranteed that it was not synthetic, not treated, nor tainted by any ethical consideration, such as is the case with conflict diamonds.

GEN Z TAKES THE LEAD

But, almost a quarter of century after the initial Bain & Co. study, when De Beers controls maybe a third of the market that it once did, brands do play a powerful role for consumers when it comes to diamonds, according to the company’s recently released Diamond Insight Report. “Trusted brands can give consumers the quality and provenance assurance they often seek while also being an expression of uniqueness and personal values,” The Diamond Insight Report stated. “So, it’s perhaps unsurprising that brands have been taking an increasing share of all diamond jewelry sales over time.”

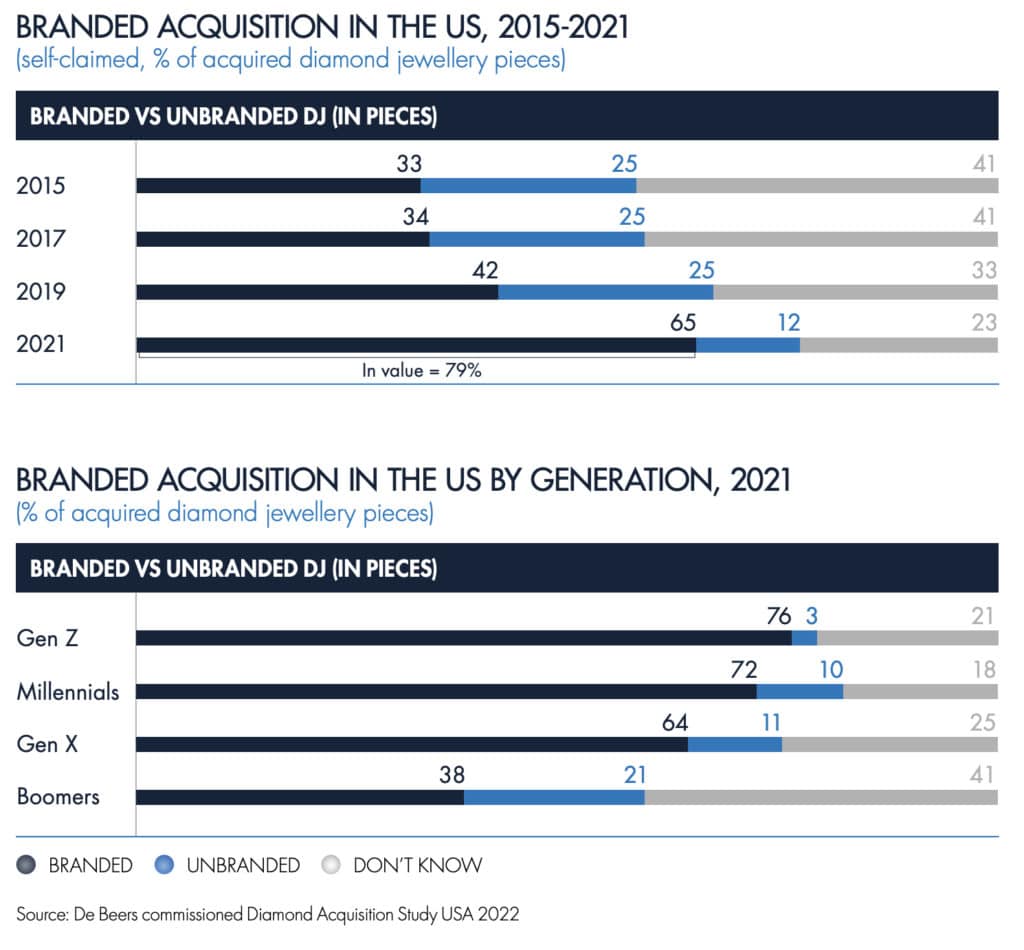

Indeed, a poll conducted for the report indicated that the popularity of brands in diamond jewelry and diamonds continues to rise. Asked whether the diamond jewelry they purchased during the course of 2021 was branded or unbranded, the American questioned said that about that two-thirds of all diamond jewelry acquisitions were branded. That was twice the proportion seen in 2015 and represents almost 80 percent of women’s diamond jewelry sales by value.

In China, brands accounted for an even higher proportion of acquisition value, with an 85 percent in 2020, the Diamond Insight report said. Gen Z is a driving force, with fully three quarters of their diamond jewelry purchases in the United States being branded in 2021, compared with two-thirds for Gen X and only a little more than one-third for Baby Boomers.

In China, brands represented 79 percent of diamond jewelry pieces purchased by Gen Z, the report stated.

LOCAL VERSUS INTERNATIONAL

There are definite factors that will influence whether a diamond jewelry brand is bought or not, with high-income consumers more likely that others to make that choice. According to the Diamond Insight Report, in the United States, some 74 percent) of diamond jewelry acquisitions by women with incomes of $150,000 or more were branded, compared with an average of nearly two-thirds (65 per cent) for all income categories.

And it not only the big-name brands that are benefitting from the trend. In the United States, the smaller local designer and retailer brands increased their growth between 2019 and 2021, attaining a 30 percent share of acquired pieces, the Diamond Insight report indicated. In contrast, international luxury diamond jewelry brands, likes of Cartier, Bulgari and Tiffany held a 17 percent share and international designer brands like Gucci and Chanel held a 13 percent share.

In China, the report stated, 66 percent of brand acquisitions were from Chinese retailers, with international brands holding only a 7 percent share.